|

Today, I wanted to do some light coverage and analysis of Tom's Hardware's reporting of Jon Peddie Research's report on GPU shipments over the same time period contrasted with Canalys' report on the size of the PC gaming market and how that's likely to affect not only GPU availability but also GPU pricing going forward...

Chronic under-supply...

There was a great article from Tom's Hardware covering Jon Peddie Research's analysis of the market over the last 10 years. Now, normally this sort of information is kept behind very expensive pay-to-access services (which is fair enough given how difficult it is to gather reliable sales/manufacturing data from various companies) so it was a fresh insight into the market we sort of take for granted, at least for me and my understanding. We normally only have access to very generalised information from these sorts of reports...

However, before we get into that, let's look at some market research from Canalys.

|

| Hmmm, seems like the market had a small dip in terms of pre-configured systems from 2010 to 2020. Note that this doesn't include the DIY market's needs... Around 61.9 M desktops shipped in 2020. [Canalys link] |

While there has been a dip in shipments of computer systems over the last ten years from the high in 2011 where there was also a high for desktop and workstation configurations of around 120 million units, here in 2020, the supply for notebooks, desktops, and workstations in total is approximately 50 million less than in 2010. Bear in mind that a lot of the systems sold post 2013 will be APU-only, coinciding with the release of Intel's NUCs and more powerful laptops onto the market with Intel mobile processors and that trend will have definitely accelerated with the release of AMD's more performant 4000 and 5000 series Ryzen APUs in the last two years.

None of these numbers include the DIY or the small integrator pre-built market* but some percentage of this total market does include desktops and laptops with dedicated GPU silicon, it's just not clear how much. Looking at Canalys' summary, Lenovo claims 24% of the market overall so maybe there's some answers there? Well, it seems like gaming laptops (which must include dedicated GPU silicon outside of an APU) account for ~10% of the total PC market in India in 2020 and I don't feel like I'm stepping out of bounds by assuming that 10% can be extended worldwide as a realistic average estimate for the laptop form factor given that Lenovo, HP, Dell and Acer take up 71% of the total market covered by this report (297 million units). This gives us an estimated number of 23.5 M laptops with dedicated GPUs...

*i.e. it will include Dell and HP but not "artisinal" small shop integrators.

... which isn't far off of the number reported by IDC for 2020 (24 million gaming laptops). IDC also helpfully disclosed the number of desktops to be around 16.7 million units for a total of 40.7 million gaming devices that would utilise dedicated graphics silicon.

|

| IDC estimates total gaming device worldwide shipments of around 40.7 million units... [IDC link] |

That's a pretty big figure, in general, but wait! There's more from the same summary of the report:

"Unfortunately, the supply of gaming PCs has tumbled recently and while crypto-mining may be partially to blame, the sheer demand for these products and growth in the player base is more likely the root cause of the shortages," said Jitesh Ubrani research manager for IDC's Worldwide Mobile and Consumer Device Trackers. "New GPUs, new games, added support for ray-tracing, and the growth in demand have also led to an increase in average selling prices during 2020 and will likely remain at these elevated levels in 2021." (Highlight is mine)

So, the number of gaming PCs and laptops shipped would have been even more than that pretty large figure if there was more stock available. Those are new systems entering the market and that figure doesn't take into account workstations for visualisaiton/CAD and/or desktops with dedicated low-to-mid-range fare that is usually sold directly to businesses...

Also, cryptomining is not the big bad wolf that many have been worrying that it is - it is putting more strain on a system which is already strained and the analysts at IDC don't expect pricing to improve right into 2022. Something Nvidia have also echoed, among others in recent days.

To recap: we have a lower-bound figure of 40.7 million (16.7 + 24) devices shipped in 2020 with a dedicated graphics die that is suitable for gaming with probably a good few million more from the devices I just outlined above... though this doesn't include discrete GPU numbers sold directly to consumers.

Jon Peddie Research, on the other hand, covered the market from a slightly different perspective, reporting that around 41.5 million discrete GPUs were shipped to the desktop PC market, specifically (according to the Tom's Hardware's coverage). Which means we can deduce that there were 24.8 million (41.5 - 16.7) discrete GPUs shipped directly to gamers as well as integrators over the same period, for a total of around 65.5 million* (40.7 + 24.8) GPU dies (across all performance and market segments) shipped in 2020.

*This number now probably includes those low-to-mid range Dell PCs I mentioned...

|

| According to Jon Peddie Research, only 60% of the volume of discrete desktop GPUs are being shipped compared to 2010, despite the market getting larger... |

The PC market and gaming market in particular is probably bigger than its ever been, with 286% in growth of concurrent Steam users since 2013 as just one indicator*, and we're entering a period where consumers are wanting to upgrade as well as join the hobby and yet we're shipping almost the lowest number of dGPUs in 10 years**? I think it is a safe bet that the market is currently under-supplied by an average of at least 40% if we assume the same marketshare as ten years ago (it's probably larger).

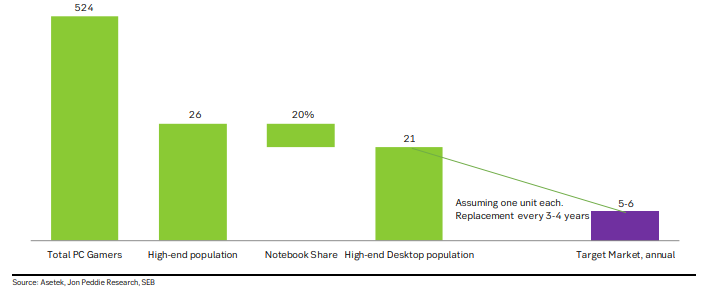

*With overall market numbers of being up 35% from 2015 in that WePC statistics page. And other reports show an overall market growth of 125% over the period of 2015-2020 for the total number of gamers - which also includes mobile and gambling. As of 2021, Asetek estimate the total PC gaming market at 524M users, with 21M being high-end desktop users and 5M high-end laptop users. Though John Peddie Research sees the total PC gaming market at around 568M...

**We're actually shipping the lowest number of GPUs since 2007 - 2006 to 2020 was the period covered by that John Peddie Research report... If we take this maximum value, we're down to only 43% of the GPUs shipped...

Worse still, the market has been under-supplied for multiple years in a row now, with expensive dGPU products that also failed to sell and it's only because of the current market conditions that those higher selling prices are being met. Many people are talking about Intel's entry to the GPU market as an almost messianic salvation but they're not far from the truth - If Intel can supply even 80% of Nvidia's yearly shipments of dGPUs (~26 M units) then we're probably good - we're back to the shipment figures we had back in 2010. Chances are that they won't do that because it will mean saturation of the market and thus lower ASPs (average selling prices) which is bad for their business but they will be supplying more than AMD can muster with their bloated catalogue of products that all compete for the same wafer supply.

But why?

It's easy to look at the numbers above and say that the market has been chronically undersupplied but the larger truth is that the demand has just not consistently been there.

|

| From John Peddie's data, it appears that most of the shortfall is coming from AMD... at least since 2014. |

When AMD and Nvidia over-produced cards during the 2016/2017 crypto boom, they were left sitting on stock they couldn't move and, in the end, both companies made fewer profits because of that. Also, if the market really was consistently calling for a higher number of cards, neither company would have reduced their output because they would have been leaving money on the table when their board partners would have been trying to obtain more stock.

The final indication that the market demand hasn't been under-supplied is that consumers have been able to freely buy graphics cards with relative ease for the duration of the last ten years.

So what's actually going on?

|

| While we're not in the holiday release period yet, and many titles have been delayed to 2022, we're getting awfully close to 1:1 CPU parity with the Xbox Series X for the average recommended specifications in the games I'm polling. We're about 60% w.r.t. the GPU... |

In my prior analysis, I showed the relationship between the recommended hardware requirements of a number of games released each year and how strong the most powerful console was at the time.

You are able to see that at the end of the PS3/Xbox 360 generation discrete graphics card performance was far in excess of what the consoles could muster. This means that, despite the poor console ports of the late 00s, gamers were able to vastly outclass the recommended requirements. However, since the PS4/Xbox One generation, that ratio has been hovering around 1 (i.e. equal to the performance of the strongest console).

I noted at the time that there's a slight lag on requirements until the year following the release of new console hardware, which also plays into what I'm about to posit.

|

| We have a slight dip in GPU recommended requirements this year (so far) but we have a lot of "tentpole" titles delayed until next year that I am fairly certain will require more beefy GPUs... |

Previously, I had thought that there were a glut of people upgrading from GTX 900 and 10 series cards alongside those who upgrade more frequently and that this was largely to blame for the additional stress on supply.

However, from this data I think that the problem is even worse than that:

- The new consoles are very graphically powerful and the latest games are requiring ray tracing features to run 'with everything turned on', along with increased rasterisation performance.

- The pandemic forced people inside and had them looking around for things to do to entertain themselves and/or perform actions they'd normally do in person (banking, education, food shopping, government-run programmes), along with working from home* (if possible).

*I am sure that not all companies gave their employees computer hardware, instead expecting them to provide their own - as a lot of these "make money at home" schemes like to do.

Combine this with the huge pressures on wafer supply dedicated to GPU production from the automotive industry and other markets as they increasingly move to incorporate more and more powerful graphics processors in their applications and we're looking at a demand spike that it seems no one really thought about ahead of time.

People who bought high end HD 5000-7000* and GTX 400-700 series cards were probably well-served by those until well into the PS4/XBO era because those consoles were so weak, and by that point they may have moved over to console gaming, reduced their PC gaming so spending money on that pastime couldn't be justified or still playing those older titles that didn't require new systems, or they moved to laptops and tablets or smartphones for their light computimg use... (bear in mind that the majority of the market do not perform DIY upgrades, they just purchase new systems)

*Specifically, the performance of an HD 7850 or above...

Also, it's important to note that, just like companies, consumers also have upgrade cycles as well. As I pointed out above, being stuck at home with a 10-year-old laptop or desktop makes you realise how poorly performant they really are. For quick, short term use they're usually fine but the majority of the "average" person's computing hardware will not have been a high-end gaming system from 2009/2010. They will not have upgraded them to use SSDs as boot drives, they won't have reinstalled windows to have a fresh start, or upgraded RAM quantities (and their RAM capacity will likely be 4-8 GB) because that consumer segment doesn't care about performance further than "it works smoothly and reliably".

It just so happens that this 10-year point was probably an effective wake-up call to finally upgrade.

|

| Small dies like the RX 6600 XT will be the answer for providing the majority of the latent demand in the market for discrete GPUs... |

So, although my estimate of the discrete GPU market being 40% under-supplied in 2020 sounds like a lot, the reality may be much, much worse. We may be looking at a cumulative under-supply* of up to 100% of current yearly market shipments for GPU dies (note, not discrete GPUs).

*Perhaps the better term would be "unrealised latent demand".

If I look a little more closely and do some back-of-the-notepad maths on what the figure might be, based on the actual deficit from 2010 shipments, I calculate it to be closer to a 70-75% - assuming that some of the unserved consumers from 2011 to 2015 were upgrading during 2016-2020. That's 138.3M d-GPUs that would have been required in 2020 for an actual shipped value of 41.50M... and this is during the extra pressure that the crypto mining craze is putting on the industry.

Assuming continued production at the same levels we've been seeing for the last couple of years, it will take around three years (from the beginning of 2020) to significantly reduce this latent demand for 70% under-supply and 1.7 years for a 40% under-supply, assuming no new consumers join the market* and that Intel enters the market with 80% of Nvidia's supply. Given that we're already 1.7 years from the beginning of 2020 and worldwide dGPU stock issues are still prevalent (though inconsistent in different countries**), it seems like we're nearing the end of unlimited AIB-consumer driven demand and instead moving towards a model of price-conscious demand - though note, there is sitll demand present, it is just not a served segment of the market at the current prices.

Currently available dGPUs are very expensive and the remaining consumers do not appear desperate enough to buy such over-priced offerings... so, it's difficult to determine where, exactly, we are in the demand spike. If the paucity of lower-end offerings continues, consumers that would have purchased a dGPU to fulfill their needs are increasingly more likely to turn to laptops for their needs, which will further release pressure on the discrete market.

*Despite the second-hand market being a thing, there are a couple of issues with this sector being able to fill the gap:

- First-off, this assumes that each primary buyer will proceed to sell their old GPU (if they even are able to when cards are broken)...

- Secondly, this assumes that the old graphics card will be performant enough to be viable for the secondary buyer

- Thirdly, this assumes that the price of the second hand card will be palatable to the secondary buyer

[UPDATE - 28 sept 2021]

- It's also come to my attention that a lot of older generations of cards are being harvested for their GDDR5 RAM, reducing the total number of second hand cards available on the market. (Broken Silicon 118, 01:58:38).

[END OF UPDATE]

**In Europe, some stock is readily available and around $100 cheaper on average (though still $200+ more expensive than MSRP) than in the USA where pretty much everything is still out of stock.

|

| An Asetek breakdown of the market, based on JPR's data... |

This can only mean that the price of GPUs will continue to be higher than the historical average for the consumer and, perhaps, exceptionally higher than the historical average for the next generation if they are released in 2022, due to the huge disparity between supply and demand.

This is going to be a painful couple of years for PC gaming!

On ther other hand, once gamers have upgraded their systems to be at least RTX 2080 Ti levels of performance (and higher), they will most likely no longer be in the market for a GPU for at least five years, perhaps longer, depending on how this generation of console devices plays out. Similarly, more average consumers will likely not require a new piece of computing hardware in the coming years once their immediate need is satiated.

At the same time, many would-be PC gamers have given up the ghost and moved to play on the current generation of consoles due to price and relative availability. So, there's probably a good portion of the market for discrete GPUs that is instead being served through that avenue...

In this light, it would be foolish for manufacturers to heed any calls to ramp up production: they would be building up a supply that could, at some unknowable point, satisfy pent-up demand and leave them holding a lot of unsellable stock, which could result in their share price tanking. Though saying that, John Peddie's latest report states that they actually are trying to increase output... increasing GPU supply by around 6.59 million discrete GPUs for the first two quarters, year-on-year. However, it seems that these efforts might be thwarted by other goings-on in and around the world...

|

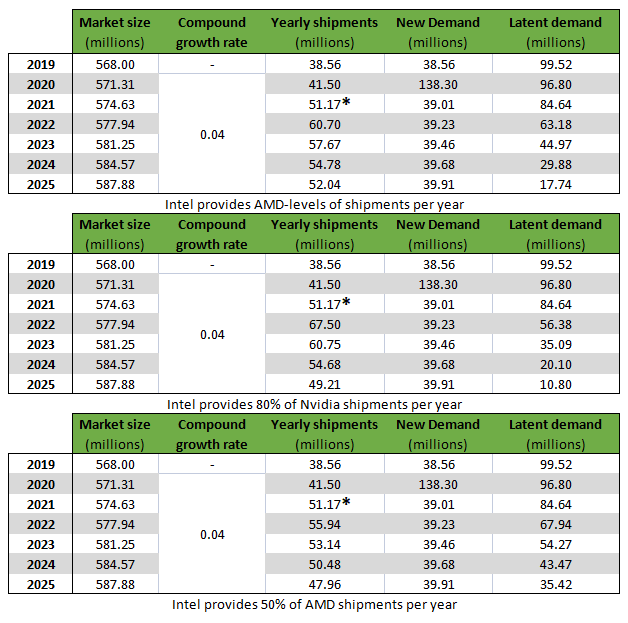

| I came up with three market predictions based on the currently available knowledge and predictions of market growth from JPR.... (*estimated 2021 shipments based on Q1 and Q2 %increase YoY) |

Knowing what I currently think I know, I put together three scenarios for the dGPU market over the next five years based on JPR's estimate of market growth for that period. I believe that for 2021 and 2022, Nvidia will increase supply in order to satiate as much demand as possible before Intel enters the market, perhaps with a primary focus on laptop and integrated solutions. It is unlikely that Intel will be entering at the mid-to-high-end performance segment in 2022, thus they will likely enable entry-level and low-end consumers to enter the market using new silicon (a segment that both Nvidia and AMD have thus far ignored).

However, I believe that while total shipments of dGPUs will peak in 2022, I forsee a gradual decline, year on year, once Intel's production capabilities and focus are clearer as the market re-adjusts to having three manufacturers and as the latent demand is slowly satiated, one way or another...

In this light, I believe that both Nvidia and AMD will limit their exposure to risk as the high-end market is catered for by their output and the low-end is primarily addressed by Intel's products.

Conclusions...

I looked at the total GPU market and the discrete GPU market, finding evidence that the market is chronically undersupplied, likely because there was very little demand for newer products during the ten year period between 2010 - 2020. I think that this is partially because the Xbox One and Playstation 4 were weak consoles in both CPU and GPU (relative to available desktop products), reducing the actual requirements of game software over the same period that probably also saw a lot of consumers move from PC to console gaming.

Similarly, many consumers who were minimally utilising older laptop or desktop hardware as home computing platforms found no reason to upgrade, with Windows 10 working well for light usage even on sytems that were purchased in 2009/2010.

This trend was reversed in 2020 due to the simultaneous release of the current generation game consoles from Microsoft and SONY alongside the global pandemic, throwing into light the poor performance of the average ancient home computing hardware being used by many consumers (and in some cases where there was zero computing hardware outside of phones or tablets available in a given home). Many homes probably also found their requirements for simultaneous computing increasing, requiring the purchase or one or more devices to fill this need.

Intel's entry into the market comes at a very important juncture where they can make a significant impact on the low-end performance segment that has a lot of as-yet unmet demand. However, depending on the size of their offering in total units shipped, we are likely to see dropping of demand for dGPUs through consumers moving to alternative computing devices instead of waiting for a dGPU solution that fits their price bracket and/or the ability to easily buy the specific product they prefer.

No comments:

Post a Comment